We no longer support this browser. Using a supported browser will provide a better experience.

发现

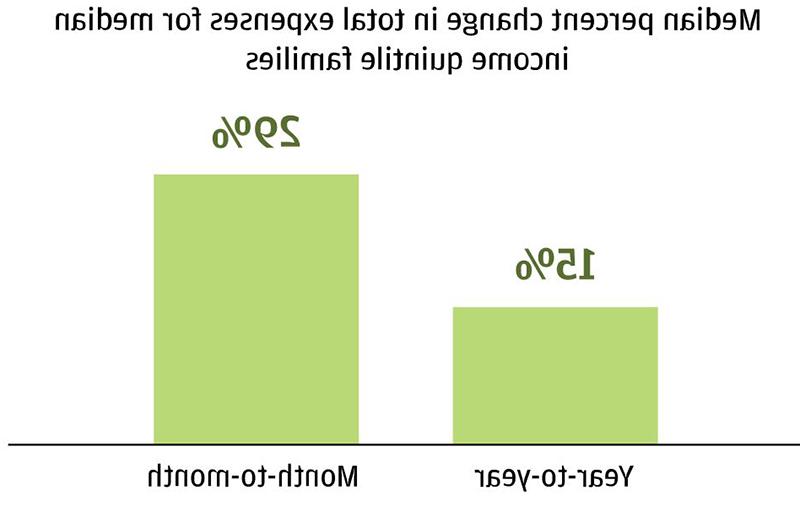

- Go to finding 1Expenses fluctuated by nearly $1,300 or 29 percent on a month-to-month basis for median-income households.

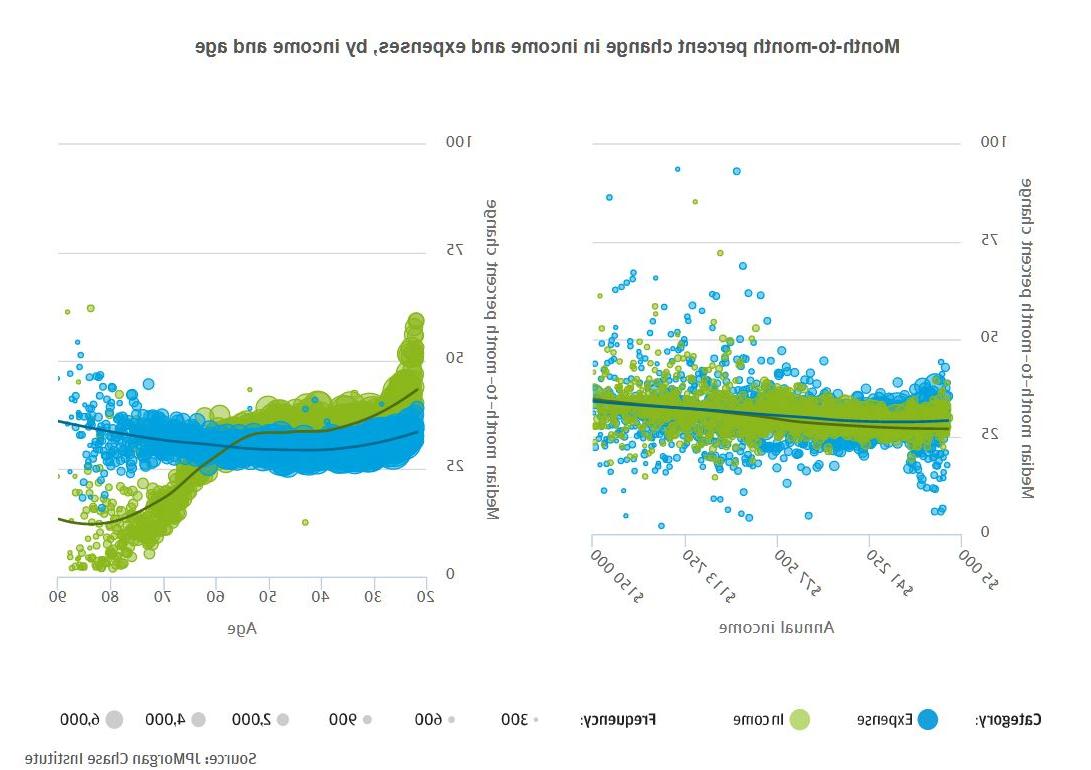

- Go to finding 2Expense volatility was high across the income and age spectrum. While older families typically had less volatile incomes, they exhibited a larger range of income and expense volatility.

- Go to finding 3几乎十分之四的家庭——尤其是中等收入和老年家庭——支付了超过1美元的额外费用,500 related to medical services, 汽车修理, 或税收.

- Go to finding 4额外的医疗支出更有可能发生在收入较高的月份,特别是在纳税季节.

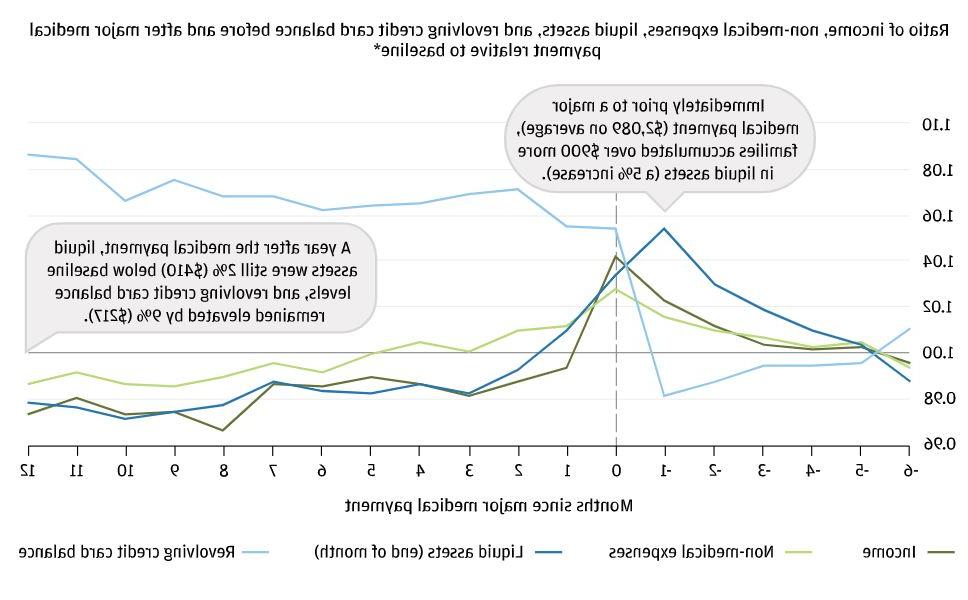

- Go to finding 5Prior to a major medical payment, 这些家庭获得了大量流动资产,但在付款后的12个月内没有恢复财务.

下载

February 2017

各个收入阶层的美国人都经历着巨大的收入和支出波动, and this volatility has been on the rise. This volatility tests the financial resilience of American families. In Weathering Volatility, we estimated that median-income families needed $4,800美元的流动资产可以抵御90%的收入和支出波动, but that they had only $3,000—a shortfall of $1,800. In Paychecks, 发薪日, 和在线平台经济我们记录了大多数收入波动源于劳动收入和, specifically, variation in take-home pay within a job rather than job transitions.

In this report, 12bet官方研究所(JP摩根 追逐 研究所)收集了近250份去身份化的数据资产,为了研究消费者的支出如何随着时间的推移而变化,以及他们的金融行为在面对特殊付款时如何变化. 这种高频家庭财务面板——加权代表了国家的年龄和收入分布——首次提供了基于真实金融交易和家庭收入变化的费用波动的组成部分, 费用, 资产, and liabilities that coincide with extraordinary medical payments.

找到一个: Expenses fluctuated by nearly $1,300 or 29 percent on a month-to-month basis for median-income households.

Finding Two: Expense volatility was high across the income and age spectrum. While older families typically had less volatile incomes, they exhibited a larger range of income and expense volatility.

Finding Three: 几乎十分之四的家庭——尤其是中等收入和老年家庭——支付了超过1美元的额外费用,500 related to medical services, 汽车修理, 或税收.

Finding Four: 额外的医疗支出更有可能发生在收入较高的月份,特别是在纳税季节.

Data

From a universe of 35 million checking account customers, we assembled a de-identified data asset comprised of roughly 250,000名核心大通客户,我们可以为他们分类至少80%的费用. These families met the following five sampling criteria:

结论

这些调查结果凸显了流动资产在管理费用飙升方面的关键作用,以及制定促进应急储蓄的政策和解决方案的必要性. 而许多家庭在支付大笔医疗费用的当月收入有所增加, 流动资产是支付医疗费用的主要资金来源. 我们的证据还强调了财务健康和身体健康之间的联系. First, the timing of medical payments was linked to ability to pay. 家庭可能会推迟治疗或支付医疗费,直到他们有能力支付. 第二个联系是,主要的医疗支出与较低的收入有关, non-medical 费用, and liquid 资产 and higher credit card debt a year later. 这突出表明,家庭没有充分投保重大健康事件的经济后果. 年龄较大的家庭尤其可以从更个性化的解决方案中受益,因为他们的收入和支出波动幅度更大,也更有可能支付大笔医疗费用. More broadly, 更好的解决方案可以帮助家庭积累流动资产并进行预测, 管理, and afford expense spikes. 集成, high-frequency data of income, 费用, 资产, 负债揭示了费用波动性以及行为如何随着这种波动性而变化. 这对于改善政策和解决方案以增强美国家庭的财务弹性至关重要.